In the tax year 2020, more than 164 million people sent their tax returns to the Internal Revenue Service. They used more than 159 million tax credit claims worth more than $277 billion to lower the amount of taxes they had to pay.

There are two ways in which tax credits can help people. A nonrefundable credit lets a taxpayer lower their income tax liability until it hits zero. A refundable tax credit lets a taxpayer reduce their income tax liability until it hits $0. They can then reduce any other taxes they owe and get a refund payment for any extra credit they are eligible for.

Individual income tax credits have steadily grown in number and value over the past few decades, as lawmakers have added new credits, made existing ones bigger, and depended more and more on the tax code to help people when the economy is bad.

In our study, we'll look at the tax credits that were claimed in tax year 2020, how the biggest tax credits were given out, and any trends in the number of tax credits and how much they were worth over time.

Taxpayers Claimed More Than $277 Billion in Tax Credits in Tax Year 2020

Most of the income that people report on their tax returns comes from pay and salaries, but people also report income from non-corporate businesses, like earnings from a partnership. So, you can get tax credits for both yourself and your business on Form 1040.

For the tax year 2020, more than 164 million taxpayers made individual income tax returns and claimed tax credits worth $277 billion. That was a big jump from the $247 billion in tax credits that were claimed in 2019. This was mostly due to the large amount of pandemic aid that was given out through the tax code in 2020.

The Child Tax Credit (CTC) had the most claims and the most money in total. The brief Recovery Rebate Credit, which helped people during the pandemic, came in second.

The Earned Income Tax Credit (EITC) and the Additional Child Tax Credit (ACTC, the refundable part of the CTC) also helped filers a lot. 26 million people claimed the EITC, which was worth a total of $59 billion, and 19 million people claimed the ACTC, which was worth almost $34 billion.

A total of $13.5 billion was claimed in school tax credits on nearly 14 million tax returns. The Foreign Tax Credit and the Retirement Savings Contributions Credit were both claimed on 9 million tax returns, but the overall amounts were very different: $1.7 billion and $21.6 billion.

Table 1. Top Tax Credits in Tax Year 2020

| Number of claims (millions) | Dollar amount of claims (billions) | |

|---|---|---|

| Child Tax Credit and Other Dependent Tax Credit | 39.3 | $84.40 |

| Recovery Rebate Credit | 31.1 | $45.40 |

| Earned Income Tax Credit | 26.0 | $59.20 |

| Additional Child Tax Credit | 19.1 | $33.70 |

| Refundable and Nonrefundable Education Credits | 13.9 | $13.50 |

| Retirement Savings Contributions Credit | 9.4 | $1.70 |

| Foreign Tax Credit | 9.2 | $21.60 |

| Other Tax Credits | 11.8 | $18.20 |

| Total | 159.9 | $277.90 |

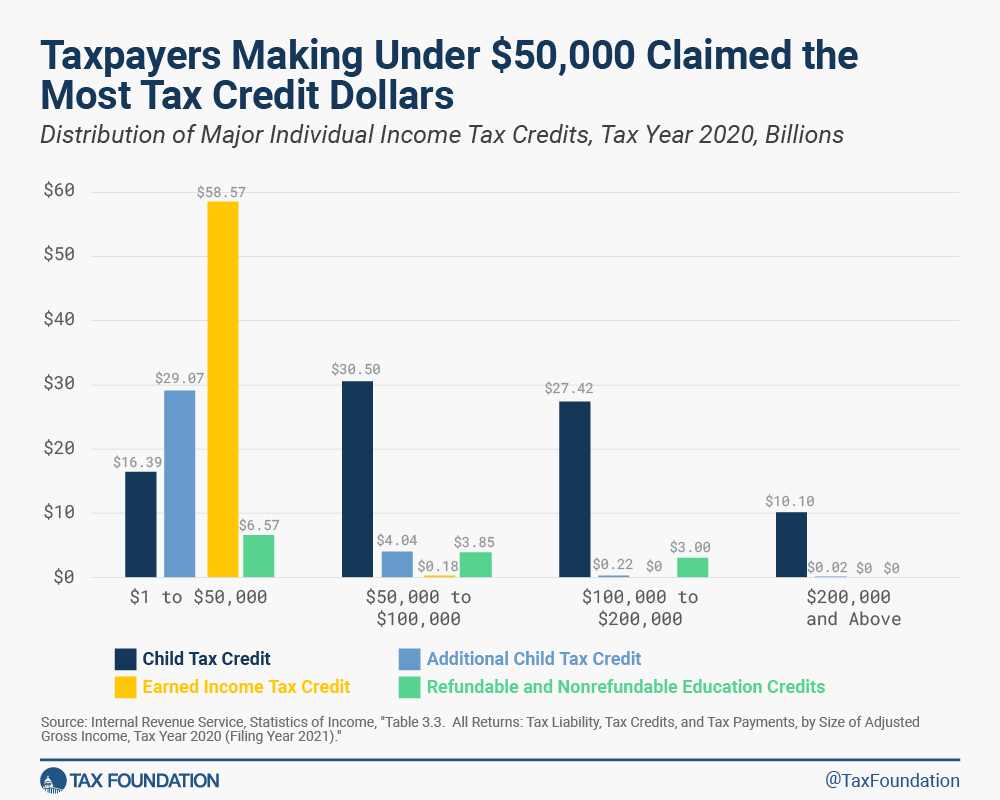

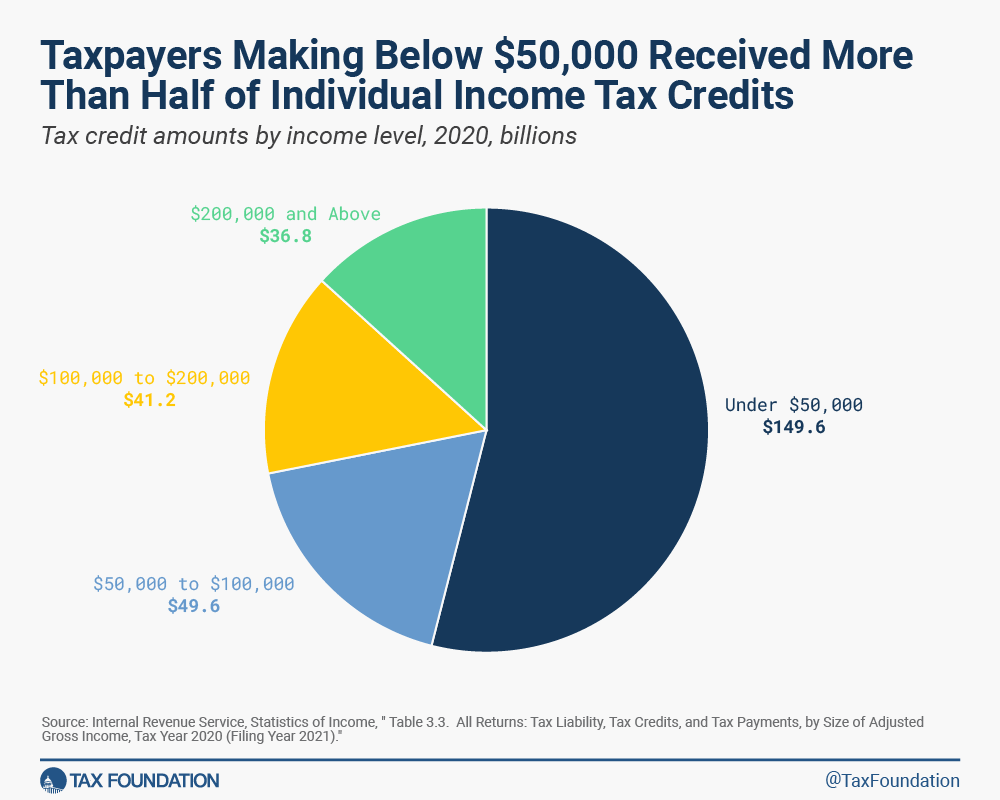

The most ACTC ($29 billion) and EITC ($59 billion) was claimed by taxpayers making between $1 and $50,000. The most prepaid CTC ($30 billion) was claimed by taxpayers making between $50,000 and $100,000, followed by taxpayers making between $100,000 and $200,000 ($27 billion). The taxpayers with the most money took the least amount of CTC and got nothing from the other three big credits.

The same pattern holds true for all $277 billion of tax credits filed on Form 1040 in tax year 2020. Taxpayers who made less than $50,000 got 54% of the tax credits they claimed, while those who made more than $200,000 got 13%.

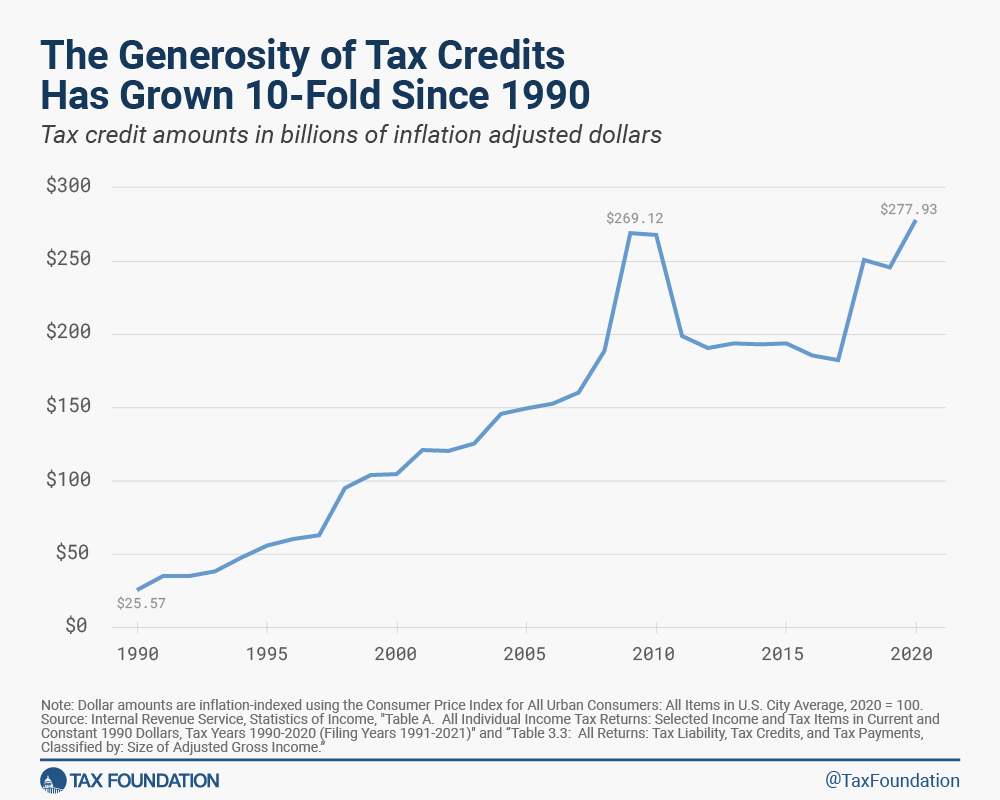

The Generosity of Tax Credits Has Grown 10-Fold Since 1990

In 1990, people made 113,7 million tax returns and claimed tax credits worth $25,6 billion (in terms of money in 2020). By 2020, 45 percent more tax returns would be made, bringing the total to 164.4 million, and tax credits would be worth $277.9 billion, 10 times more than they were in 2000.

The value of tax credits has gone up both when the economy was good and when it was bad. As the chart to the right shows, the biggest jumps happened when the economy was bad or when there was a big tax change. For example, the biggest reason for the rise from 2007 to 2009 was the Recovery Rebates in 2008 and the Making Work Pay Credit in 2009. In the same way, the expansion of the CTC in the 2017 tax reform caused a big jump in 2018, and pandemic relief programs in 2020 caused another big jump in the overall value of tax credits claimed through recovery rebates (since the American Rescue Plan didn't expand the CTC until 2021).

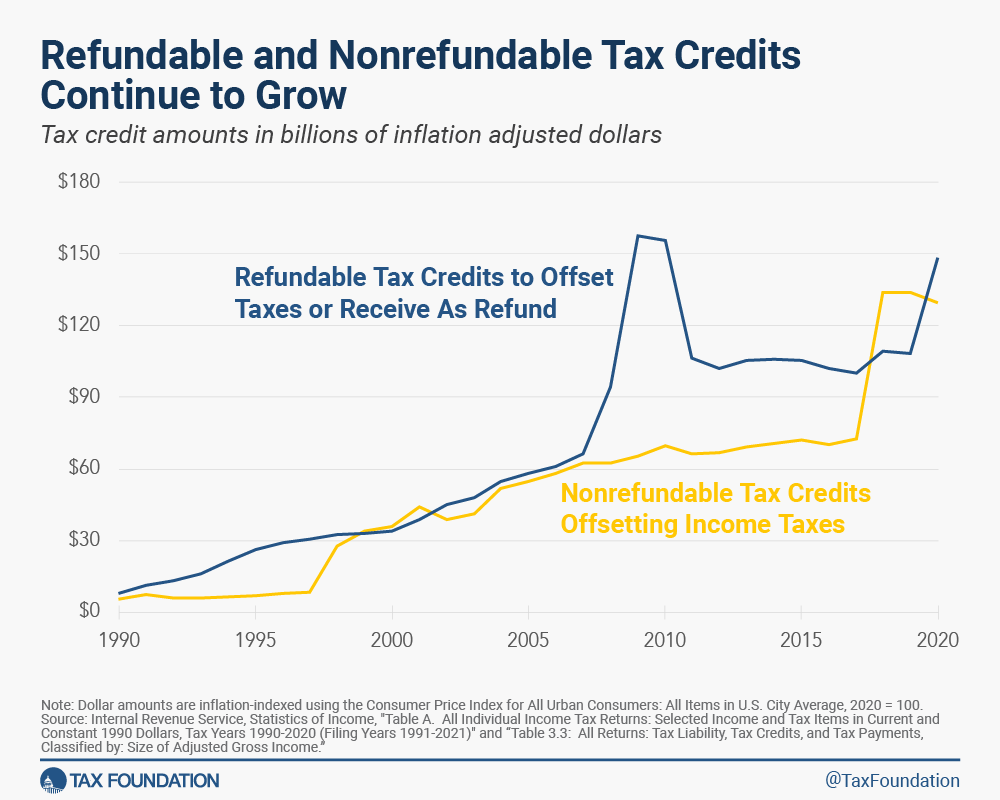

Before credits, the IRS says that the total amount of income tax due on tax forms for 2020 was $1.83 trillion. $129 billion in income taxes are offset by tax benefits that can't be refunded. More than $21 billion in income taxes and almost $11 billion in other taxes were cancelled out by credits that could be refunded. This left a net return of $116 billion. For tax year 2020, both refundable and non-refundable tax credits added up to more than $277 billion.

From 1990 to 2020, refundable tax credits have made up an average of 60% of all tax credits, while nonrefundable tax credits have made up an average of 40% of all tax credits. From 1990 to 2020, there were only five years when nonrefundable tax credits were worth more than refundable tax credits. Those years were 1999, 2000, 2001, 2018, and 2019.

Based on papers from the IRS, the Congressional Research Service, or the General Accountability Office, Table 2 gives short descriptions and important dates for each of the 28 types of tax credits listed in IRS Statistics of Income Table A.

Table 2. Descriptions of Individual Income Tax Credits

| Name of Credit | Relevant dates | Description |

|---|---|---|

| Additional Child Tax Credit | Made refundable in 2001 | Refundable portion of the CTC of up to $1,400 (adjusted for inflation with a $2,000 limit) per eligible child. |

| Adoption Credit | Created in 1996, available beginning in 1997 | A nonrefundable credit to offset the cost of adoption related expenses for families who adopted or began the adoption process in 2020. The maximum credit is $14,300 for each eligible child under the age of 18 and begins to phase out when modified AGI exceeds $214,520. |

| Advance Earned Income Credit Payments | 1979-2010 | Beginning in 1979, workers could elect to receive the EITC in advance payments along with their paychecks. The advance payment option ended for tax years beginning after December 31, 2010. |

| Alternative Fuel Vehicle Refueling Property Credit | Created in 2005 | A nonrefundable credit for taxpayers who install “qualified vehicle refueling and charging property” in their home or place of business. The credit is equivalent to 30% of the expense of qualifying property and limited to a maximum of $30,000 per location for business property and $1,000 per location for non-business property. |

| Alternative Motor Vehicle Credit | Created in 2005 | A nonrefundable tax credit claimed on Form 8910 to offset the cost of purchasing a vehicle with at least four wheels that uses alternative energy sources. |

| American Opportunity Credit | Created in 2009 | The refundable portion of the AOTC is reported separately in the IRS data. |

| Child and Dependent Care Credit | Created in 1976 | Allows a nonrefundable tax credit for child or dependent care expenses incurred while working or looking for work. The maximum credit varies by income level and equals up to 35% of up to $3,000 in eligible expenses for one qualifying dependent or up to $6,000 in eligible expenses for more than one qualifying dependent. |

| Child and Other Dependent Tax Credit | Created in 1997, available beginning in 1998 | Allows a credit for “qualifying children” under the age of 17 claimed as a dependent on an individual's tax return. The credit allows up to $2,000 for each child to offset income taxes due. A nonrefundable credit of $500 is also available for dependents not eligible for the child tax credit. The credit phases out at 5% when AGI exceeds $200,000 for single filers and $400,000 for joint filers. See Additional Child Tax Credit for information on the refundable portion. |

| Credit for the Elderly or Disabled | Renamed from “Retirement Income Tax Credit” to “Credit for the Elderly” in 1976, added reference to disabled in 1983 | A nonrefundable credit of up to $1,125 for individuals 65 years of age or older or retired on permanent and total disability who meet certain income requirements. |

| Credit for Federal Tax on Gasoline and Special Fuels (Form 4136) | In 1956, Congress provided that Treasury refund taxes paid on gasoline used on farms for farming purposes and certain other non-highway purposes be refunded. | A refundable credit claimed on Form 4136 for taxpayers who paid federal excise tax on gasoline or special fuels for certain purposes. |

| Earned Income Credit | Created in 1975 | A refundable tax credit for taxpayers with earned income. Maximum amounts vary by number of qualifying children: $538 for no qualifying children, $3,584 for one, $5,920 for two, and $6,660 for three or more. Not available to taxpayers with investment income above $3,650. |

| Education Credits: American Opportunity Tax Credit (AOTC) and Lifetime Learning Credit (LLC) | AOTC created in 2009 | The AOTC allows eligible students to receive a maximum annual credit of $2,500 and a refund of 40% (up to $1,000) of any remaining amount of the credit if the credit reduces tax liability to zero. The credit can only be used for the first four years of postsecondary education and phases out for AGI between $80,000 to $90,000 for single filers and $160,000 to $180,000 for joint filers. |

| LLC created in 1997 | The LLC is a nonrefundable credit for qualified tuition and related expenses of eligible students enrolled in an educational institution and is worth up to $2,000. The credit phases out for AGI between $59,000 to $69,000 for single filers and $118,000 to $138,000 for joint filers. Only one education credit can be claimed per eligible student. | |

| First-Time Homebuyer Credit | 2008-2010 | A fully refundable credit of up to $8,000 for homes purchased from 2008 to 2010. Homebuyers who purchased homes in 2008 had to repay the credit over a period of up to 15 years. |

| Foreign Tax Credit | Created in 1918 | Can be claimed as a credit or itemized deduction intended to reduce U.S. taxable income or liability for individuals who paid or accrued foreign taxes in a foreign country or U.S. possession. Form 1116 must be completed if the credit is greater than $300 (or $600 for married taxpayers filing jointly). |

| General Business Credit | Varying dates | Limited to 100% for the first $25,000 of tax liability ($12,500 for married couples filing separately) and 25% of any excess tax liability over $25,000. Any excess amount of the business credit for the current year can be carried forward 20 years. |

| Taxpayers use the General Business Credit when they claim more than one of the following tax credits: investment credit; research credit; low-income housing credit; disabled access credit; renewable electricity, refined coal, and Indian coal production credit; Indian employment credit; orphan drug credit; new markets credit; small employer pension plan startup credit; employer-provided child care facilities and services credit; biodiesel and renewable diesel fuels credit; low-sulfur diesel fuel production credit; distilled spirits credit; nonconventional source fuel credit (carryforward only); energy-efficient home credit; energy-efficient appliance credit (carryforward only); alternative motor vehicle credit; alternative fuel vehicle refueling property credit; enhanced oil recovery credit; mine rescue team training credit; agricultural chemicals security credit (carryforward only); credit for employer differential wage payments; carbon dioxide sequestration credit; qualified plug-in electric drive motor vehicle credit; qualified plug-in electric vehicle credit (carryforward only); employee retention credit; new hire retention credit (carryforward only); credit from electing large partnerships (carryforward only); oil and gas production from marginal wells credit; and, certain business credits allowed against the Alternative Minimum Tax. | ||

| Health Coverage Tax Credit (Form 8885) (Formerly the Health Insurance Credit) | Created in 2002, sunset January 1, 2022 | A refundable credit to assist certain displaced workers and retirees to cover health insurance premiums. It expired on December 31, 2021. |

| Making Work Pay Credit | Available for 2009 and 2010 | A refundable tax credit of up to $400 for single filers and up to $800 for joint filers, provided in tax years 2009 and 2010. |

| Mortgage Interest Credit | Created in 1984 | Allows a nonrefundable credit for taxpayers who received a qualified Mortgage Credit Certificate (MCC) from a State or local government. |

| Net Premium Tax Credit | Created in 2013, available beginning in 2014 | A refundable credit that helps eligible individuals and families pay for health insurance premiums purchased through the Health Insurance Marketplace. |

| Prior-Year Minimum Tax Credit | Congress enacted the AMT in 1969 | A nonrefundable credit to offset alternative minimum tax (AMT) paid in 2019 or prior years. |

| Qualified Electric Vehicle Credit | Created in 2005 | A nonrefundable credit for taxpayers who are eligible for qualified electric vehicle passive activity credits for the current tax year, applied to previous years. |

| Qualified Plug-In Electric Vehicle Credit | Created in 2008 | A nonrefundable credit for any qualified, non-depreciable plug-in electric vehicle that was put into service during the tax year, worth up to $7,500. |

| Qualified Sick and Family Leave Credit | Created for the COVID-19 pandemic in 2020 | A refundable tax credit for eligible small and medium-sized businesses to reimburse the costs of providing qualified sick and family leave wages to employees for periods of leave during the COVID-19 pandemic. |

| Recovery Rebate Credit | 2008, 2020, 2021 | A refundable credit for individuals who did not receive or received less than the full amount of the Economic Impact Payments worth up to $1,200 for single filers or $2,400 for joint filers in the first round and $600 for single filers or $1,200 for joint filers in the second round. |

| Refundable Prior-Year Minimum Tax Credit (Form 8801) | 2007-2013 | A refundable credit for taxpayers with a credit carryforward from earlier years, no longer available after 2013. |

| Regulated Investment Company Credit (Form 2439) | Tax treatment of RICs most recently reformed with the Regulated Investment Company Modernization Act of 2010 | A refundable credit claimed on Form 2439 for taxes already paid on undistributed long-term capital gains. |

| Residential Energy Credit | First introduced in the 1970s, expired in 1985, reintroduced in 2005, currently set to expire in 2032 | Consists of the non-business energy property credit and the residential energy-efficient property credit. |

| The non-business energy property credit allows 10% of the costs paid or incurred in 2020 for qualified energy-efficient residential improvements and residential energy property limited to a $500 lifetime total. | ||

| The residential energy-efficient property credit is a credit of 26% for homeowners who invested in renewable energy for their home in the form of solar, wind, geothermal, fuel cells, or battery storage technology. | ||

| Retirement Savings Contributions Credit | Created in 2002 | Allows a maximum credit of $1,000 (or $2,000 if married filing jointly) for qualified retirement savings contributions if AGI is below $32,500 for single filers, $48,750 for head of household filers, or $65,000 for joint filers. |

Source: Tax Foundation summaries of Internal Revenue Service, Congressional Research Service, General Accountability Office, and relevant legislation.