Uncle Sam can tax up to 85% of your Social Security benefits if you have other sources of income, such as earnings from work or withdrawals from tax-deferred retirement accounts.

Many people are surprised to learn that Social Security benefits can be taxed. After all, why is the government sending you a payment one day and asking for some of it back the next? But if you take a closer look at how the federal tax on Social Security is calculated, you'll see that many people actually don't pay any tax on their Social Security benefits.

There's no federal income tax on Social Security benefits for most people who only have income from Social Security. Thanks to the highest cost-of-living adjustment in 40 years, the average monthly Social Security check for a retired worker in 2022 is $1,658, which comes to $19,896 per year. That's well below the minimum amount for taxability at the federal level.

On the other hand, if you do have other taxable income — such as from a job, a pension or a traditional IRA — then there's a much better chance that Uncle Sam will take a 50% or 85% bite out of your Social Security check. Plus, depending on where you live, your state might tax a portion of your Social Security benefits, too.

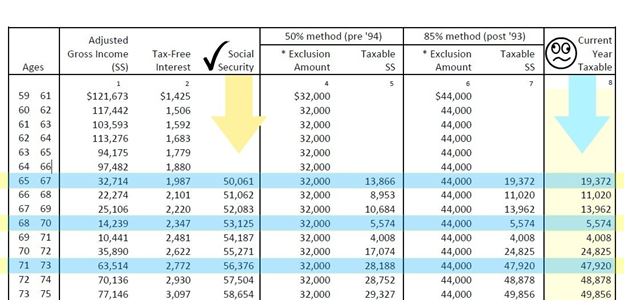

Once you start collecting Social Security benefits, you'll get a Social Security benefits statement (Form SSA-1099) in the mail each year in January showing the total amount of benefits you received in the previous year. To figure out how much, if any, of the total amount may be taxed, the first thing you need to do is calculate your "provisional income." Your provisional income is generally equal to the combined total of (1) 50% of your Social Security benefits, (2) your tax-exempt interest, and (3) the other non-Social Security items that make up your adjusted gross income (minus certain deductions and exclusions).

For single people, your Social Security benefits aren't taxed if your provisional income is less than $25,000. The threshold is $32,000 if you're married and filing a joint return. If your provisional income is between $25,000 and $34,000 for a single filer, or from $32,000 to $44,000 for a joint filer, then up to 50% of your Social Security benefits may be taxable. If your provisional income is more than $34,000 on a single return, or $44,000 on a joint return, up to 85% of your benefits may be taxable.

:max_bytes(150000):strip_icc()/GettyImages-963811020-4a28b09314ec43108714573b93e1fcae.jpg)

Social Security Income | Internal Revenue Service

Social security benefits include monthly retirement, survivor and disability benefits. They don't include supplemental security income (SSI) payments, which aren't taxable. The net amount of social security benefits that you receive from the Social Security Administration is reported in Box 5 of Form SSA-1099, Social Security Benefit Statement, and you report that amount on line 6a of Form 1040, U.S. Individual Income Tax Return or Form 1040-SR, U.S. Tax Return for Seniors. The taxable portion of the benefits that's included in your income and used to calculate your income tax liability depends on the total amount of your income and benefits for the taxable year. You report the taxable portion of your social security benefits on line 6b of Form 1040 or Form 1040-SR.

Your benefits may be taxable if the total of (1) one-half of your benefits, plus (2) all of your other income, including tax-exempt interest, is greater than the base amount for your filing status.

If you're married and file a joint return, you and your spouse must combine your incomes and social security benefits when figuring the taxable portion of your benefits. Even if your spouse didn't receive any benefits, you must add your spouse's income to yours when figuring on a joint return if any of your benefits are taxable.

Generally, you can figure the taxable amount of the benefits in Are My Social Security or Railroad Retirement Tier I Benefits Taxable?, on a worksheet in the Instructions for Form 1040 (and Form 1040-SR) or in Publication 915, Social Security and Equivalent Railroad Retirement Benefits. However, if you made contributions to a traditional Individual Retirement Arrangement (IRA) for 2022 and you or your spouse were covered by a retirement plan at work or through self-employment, use the worksheets in Publication 590-A, Contributions to Individual Retirement Arrangements (IRAs), to see if any of your social security benefits are taxable and to figure your IRA deduction.

The amount of income tax that your child must pay on that part of the benefits that belongs to your child depends on the child's total amount of income and benefits for the taxable year.