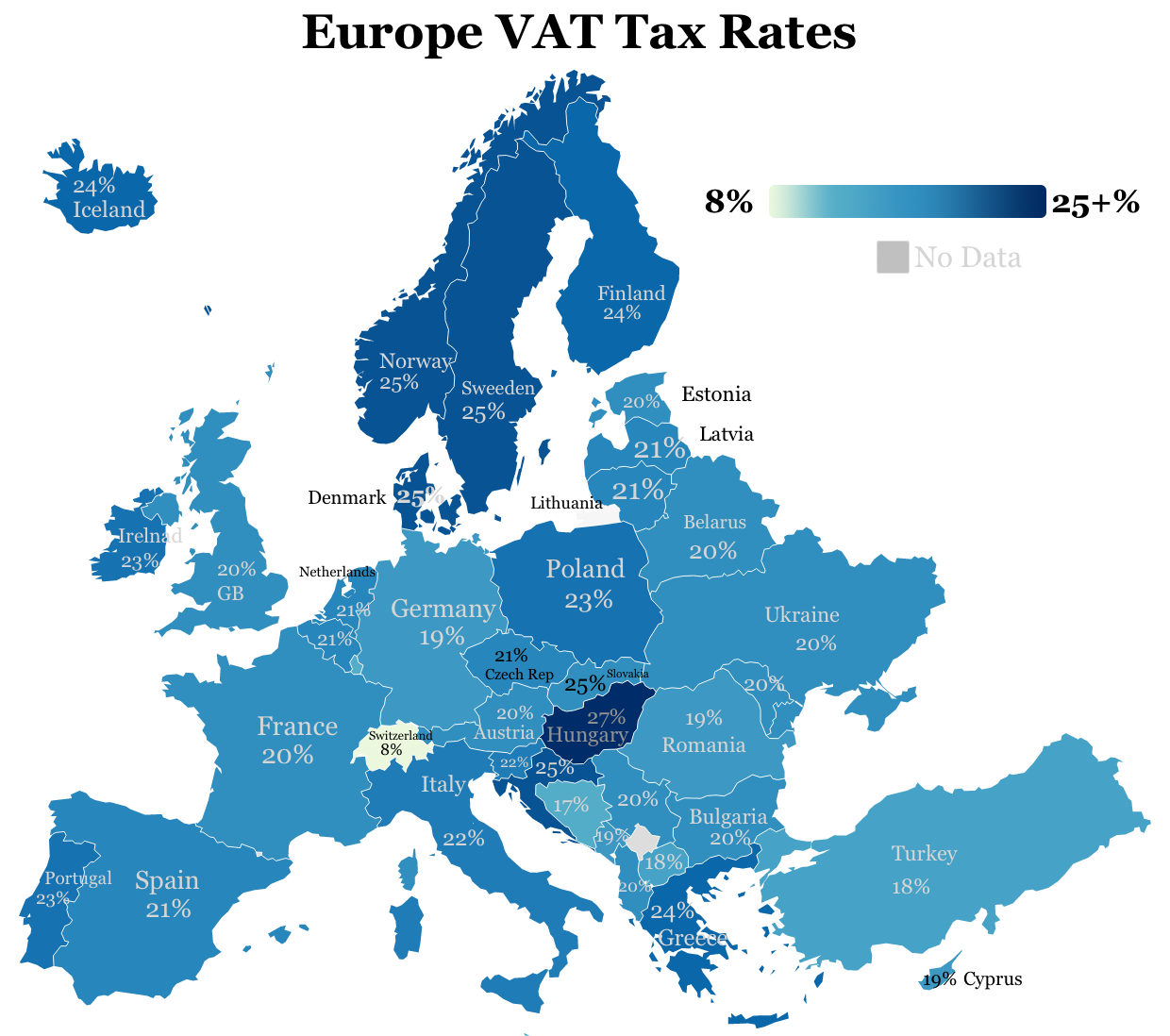

'The criteria of simplicity, transparency, predictability, and justice should be met by new own resources.'

The aforementioned advice seems to have come from a Tax Foundation research on a morally sound EU own resources strategy. Although we would like to take credit, the advice was first provided in the EU's 2016 Monti report and more recently in the 2020 Institutional Agreement on new own resources.

Governments can generate enough money, support the economy, and create a successful tax system when policy is created based on these fundamental ideas. Governments, consumers, and businesses all profit from the recent EU VAT change on e-commerce.

The EU decided to end the VAT exemption on items imported into the EU by non-EU businesses that are valued at less than €22 in July 2021. In other words, customers will now pay the same tax regardless of the value of the commodity or whether the e-seller is from the EU because a carveout was eliminated and the tax base was expanded.

The EU calculated that importers were abusing the exemption by intentionally lowering the price of their goods below the exemption threshold, costing EU coffers up to €7 billion annually. Government budgets were harmed as a result of the increased tax burden placed on taxpayers importing more expensive or substantial amounts of products.

When the fraud was discovered by authorities, EU clients would get a call from customs after the product had been delivered to their home, requesting the additional VAT payment. Many customers were surprised by the added expense.

Additionally, non-EU businesses were unfairly obtaining a competitive edge against EU businesses who were unable to take use of the tax exemption.

The reform also addressed issues with corporate compliance. Before July 2021, vendors had to register for VAT in each Member State when their annual sales exceeded a predetermined threshold. The cutoff varied from nation to nation.

By replacing the multiple thresholds with a single, €10,000 EU-wide level, the change made this requirement simpler. Additionally, online vendors can now sign up for the "One Stop Shop," an electronic platform where they can manage all of their VAT requirements for transactions made across the EU.

To help importers register for VAT in the EU and make sure the right amount of VAT is paid to the right Member State, a comparable system known as the "Import One Stop Shop" was put into place.

How well has the reform performed two years later? Is the VAT system for online sales simpler, more transparent, more predictable, and more equitable?

Recent findings indicate that the answer is indeed.

In 2022, Member States received about €20 billion in VAT receipts. This sum comprises €17 billion from the One Stop Shop (OSS) portal's expanded use as well as €2.5 billion in VAT receipts from the importation of e-commerce products. Additionally, it includes the recently introduced VAT revenues for packages with a value of less than €22, which were prone to fraud. Overall, compared to 2021 statistics, VAT revenues received through these newly established systems increased by 26%.

We now have a more complete picture of the effects and effectiveness of the EU's VAT regulations for the reform of e-commerce. The previous two years have shown evidence of effective tax policy in action: by removing carveouts to broaden the base and streamlining reporting and compliance requirements for businesses and consumers, the tax burden has been made more manageable and revenues have increased.

8,000 traders had registered in the new system six months into the reform. Today, there are over 130,000 registered companies under the new system.

While the old system was enhanced by the VAT e-commerce reform, several other parts of the VAT have taken a step backward. The Council formally authorized changes to the list of products and services that are eligible for reduced VAT rates in April 2022. In other words, despite negligible benefits to consumers and more complicated tax laws, more carveouts can now be adopted. The strategy also undermines the value of the VAT as a revenue stream.

Instead of using tax fairness as a euphemism for income inequality or corporate profitability, policymakers should continue to rely on these guiding principles as the EU considers additional reforms to the VAT system, including the VAT in the Digital Age proposal (ViDA) and other new own resources. It is simpler to determine whether the tax system is fair when the regulations are plain and clear. The EU and its member states can cooperate to boost economic growth and increase income at the same time.