In the past few years, countries have talked about making big changes to the tax rules that affect multinational businesses.

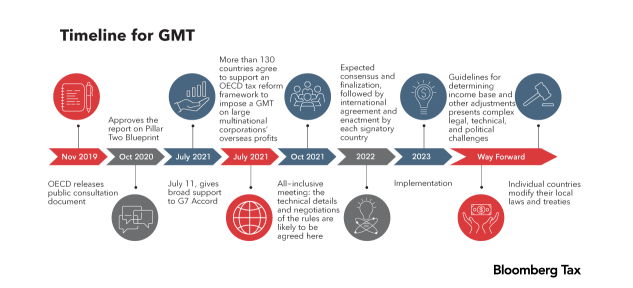

After talks at the Organization for Economic Co-operation and Development (OECD), more than 130 countries will have agreed on a plan for new tax rules by October 2021.

Large companies would pay more taxes in countries where they have customers and less in countries where they have their headquarters, workers, and operations. The agreement also sets a global minimum tax of 15%, which would raise taxes on businesses that make money in places with low taxes.

Governments are currently making plans for putting the deal into action and making it a law.

The OECD's plan is based on a plan that has been talked about since 2019. The change is built on two "pillars": Pillar One changes where big companies pay taxes, which will affect their profits by about $125 billion. Pillar Two creates a global minimum tax, which will bring in an expected $150 billion more in taxes around the world.

Due to problems with implementation and disagreements about policy details, the final copy of a multilateral treaty on Pillar One won't be ready until mid-2023, and Pillar Two won't be ready until at least 2024.

Pillar One has a "Amount A" that applies to businesses with more than €20 billion in sales and a profit margin of more than 10%. Some of these companies' profits would be taxed in places where they do business. For example, 25% of earnings over a 10% margin could be taxed. After seven years of review, the €20 billion limit could be lowered to €10 billion.

Amount A is a limited redistribution of tax money from countries where big multinational companies operate to countries where they have customers. A large number of these companies are based in the United States.

This plan could cause the U.S. to lose tax money. But U.S. Treasury Secretary Janet Yellen has said in the past that she thinks Amount A would have little effect on U.S. income. But for this to be true, the U.S. would need to get a lot of money from foreign companies or from U.S. companies with foreign offices that sell to U.S. buyers.

Recent drafts of rules show where companies will pay taxes under Amount A. Even when a company sells to another business in a long supply chain, there are ways to find out who the end consumers are. The proposed rules also let companies decide how to spend their taxable income based on macroeconomic data about how much people spend.

Pillar One also has "Amount B," which makes it easier for companies to figure out how much tax they have to pay on things like selling and marketing in other countries.

The global minimum tax is the second part. It has three main rules and a fourth rule for international tax agreements. Companies with more than €750 million in sales should follow these rules. In December 2021, model rules were made public.

The first is a "domestic minimum tax," which countries could use to claim the right to tax income that are currently taxed at less than 15%.

The second is an Income Inclusion Rule, which says when a company's foreign income should be added to the parent company's taxed income. The deal sets the minimum effective tax rate at 15%. If it is lower than that, the company's home country would have to pay more taxes.

The income inclusion rule would apply to foreign profits after taking out 8% of the value of tangible assets (like tools and buildings) and 10% of payroll costs. Over the course of 10 years, these payments would be cut down to 5% each.

Importantly, Pillar Two rules rely mostly on financial (or "book") accounting data rather than tax accounting data. Because of these timing gaps between the books and taxes, the Pillar Two rules focus on deferred tax assets, such as net operating losses and capital allowances. But the minimum tax rate of 15% must be used to value these deferred tax assets.

Like other rules that tax foreign earnings, the income inclusion rule will raise the tax costs of cross-border investment and change how businesses decide where to hire and spend around the world, including in their own operations.

The Undertaxed Profits Rule is the third rule in Pillar Two. It says that a country can raise taxes on a company if another related business in a different country is taxed at a rate lower than 15%. If a similar top-up tax is used in more than one country, the taxable profit is split based on where the tangible assets and workers are located.

Together, the domestic minimum tax, the income inclusion rule, and the Undertaxed Profits Rule impose a minimum tax on both companies that invest abroad and foreign companies that invest in the United States. All of them are tied to a minimum effective rate of at least 15% and would be used in every place where a company does business.

The fourth rule of Pillar Two is the "subject to tax rule." This rule is meant to be used in a tax treaty framework to let countries tax payments that might only be taxed at a low rate otherwise. With this rule, the tax rate would be set at 9%.

For Pillar One to work, every country must follow the same rules. This would stop companies from having to deal with different methods in different parts of the world.

Pillar Two is less important. The form of Pillar Two that has been outlined is like a template that countries can use to make their own rules. If enough countries follow the rules, a big chunk of company profits around the world would be subject to a tax rate of 15%.

Both Pillar One and Pillar Two are big changes to the way taxes are done around the world. As part of Pillar One, the plan says that taxes on digital services and other policies like them will need to be taken away. The U.S. Trade Representative has talked with some countries that have taxes on digital services to make sure the change goes smoothly. Countries would need to write new laws, change the language in their tax treaties, and get rid of policies that go against the new rules.

After months of talks, everyone in the European Union (EU) decided that Pillar Two should be put into place. By the end of 2023, the EU Directive will have to be written into the laws of each country. Starting in 2024, companies with an annual sales of at least €750 million will have to pay the minimum rate of 15%. This includes domestic groups that make enough money to meet the requirement.

Member States with more than 12 in-scope multinational groups must adopt the Income Inclusion Rule by December 31, 2023, and the Undertaxed Profits Rule by December 31, 2024. Member States with less than 12 people can choose to put off putting both rules into place for six years.

As of May 30, 2023, 11 countries around the world have either proposed or passed laws that put Pillar Two's model rules into their own national laws. Also, Switzerland will vote on whether or not to follow the rules on June 18 in a poll.

Congress hasn't made any changes yet that are in line with the global tax deal. Congress left these changes out of the 2022 Inflation Reduction Act, even though the Biden administration backs the deal. Also, Representative Jason Smith (R-MO), who is the head of the House Ways and Means Committee, recently proposed retaliatory legislation that would go against foreign laws that apply minimum tax rules to American multinationals.

Tax treaties need 67 votes in the Senate to be ratified, which makes it hard to pass Pillar One without backing from both sides of the political aisle.

If U.S. policy doesn't change, U.S. companies will be caught in a confusing web of minimum taxes, such as the Global Intangible Low-Tax Income (GILTI), the Base Erosion and Anti-Abuse Tax, the new Corporate Alternative Minimum Tax from the Inflation Reduction Act, and probably some of the global minimum tax rules. Recent advice on Pillar Two means that U.S. GILTI would be applied after foreign minimum taxes. This would mean that this policy would bring in less tax money for the U.S.

The way the rules are set up means that when the EU adopts them, it has a huge effect on global companies all over the world. It also puts pressure on other countries to follow some form of the rules or to change their tax codes in some other way.

The rules make it clear that businesses should get assistance to make up for some of the extra costs caused by the minimum tax. This is because standard tax credits aren't as good as government handouts and refundable tax credits.

The agreement will have a big effect on tax competition, and many countries will have to rethink how they tax international companies. Now that the EU has made a change, many businesses will start getting ready to follow the policy in 2024. If Pillar One doesn't work, we could go back to a world with unfair taxes on digital services in Europe and reciprocal tariffs in the US.