How bond market mayhem set off a pension ‘time bomb’

As they made their pitch to overhaul the pension scheme of one of Britain’s biggest retailers, Next chief executive Lord Simon Wolfson remembers the consultants were “very sure of themselves”.

“Liability-driven investing”, the consultants promised, was a stress-free way to protect the fund from swings in interest rates by using derivatives.

There is one particular phrase that still sticks in Wolfson’s mind from the 2017 meeting: “You put it in a drawer, lock the drawer and forget about it.”

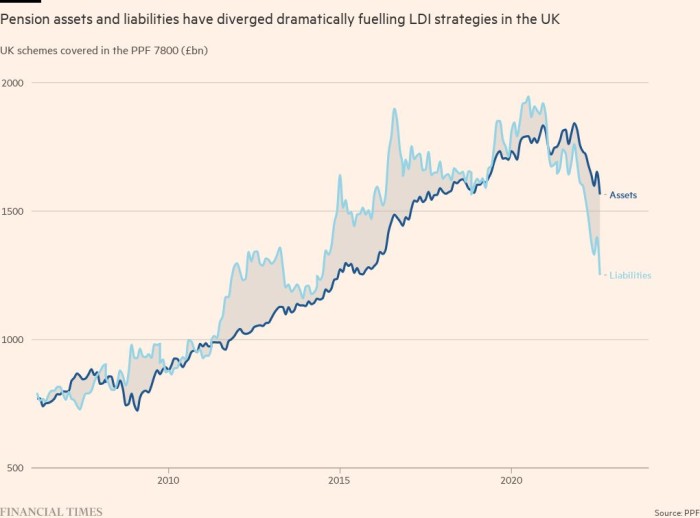

Schemes and asset managers say that, in the market environment that has characterised the past two decades, it has proved effective. A global bull market for bonds pushed up prices and drove down yields, meaning that pension funds who were unhedged against these moves would have found themselves trying to generate returns to meet ever-increasing liabilities. The lack of hedging or insufficient hedging at companies such as construction group Carillion and retailer Arcadia Group were contributing factors to their ensuing insolvency, according to pensions experts.

Professional services firm PwC estimates that pension funds have moved from a £600bn deficit a year ago to a £155bn surplus; liabilities have halved from £2.4tn to £1.2tn. More than 20 per cent of UK DB pension funds were in deficit in August this year, and more than 40 per cent were a year earlier, according to the BoE.

“LDI saved schemes from untenably large deficits and it saved sponsors from constantly topping up schemes,” said Andy Connell, head of solutions at Schroders, which has $55bn in its global LDI business. “They were able to keep cash in the business for wages, investment and dividends. LDI strategies have been a great societal good for UK plc and the economy.”

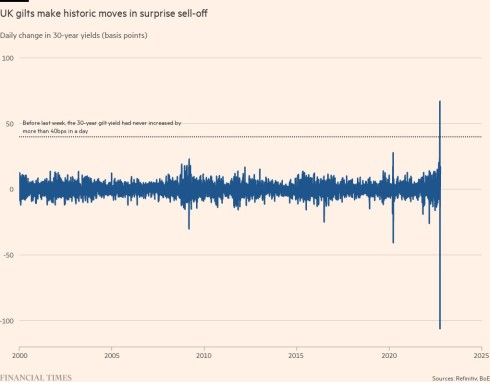

Although the BoE’s intervention calmed the market, it did not end pension schemes’ dash for cash. Counterparties have demanded more collateral to de-risk the derivatives. And there is a fear that when the BoE’s two-week bond-buying programme ends next week, volatility will return.

“We are seeing a lot of activity that would normally take months in the pension fund world being done in a matter of days,” said Calum Mackenzie, an investment partner at consultant Aon. “That’s putting a huge strain on to the system.”

Nikesh Patel, head of client solutions at Van Lanschot Kempen, reckons that pension schemes in aggregate will have to come up with as much as £280bn to fully recapitalise their interest rate and inflation hedges with new lower levels of leverage. This is in addition to the £200bn that schemes have already had to deliver to meet LDI collateral calls.

One option is to jettison the LDI strategies altogether but that leaves pension schemes exposed to future swings in rates and inflation.

Sonja Laud, chief investment officer at LGIM, says: “Early indications suggest that most of our clients want to keep their hedge ratio intact and provide us with more collateral.”

Trustees who can be held personally liable for pension losses are being asked to hurriedly approve asset sales even though the exact funding position of many schemes remains unclear as a result of the recent market volatility.

In a memo seen by the FT, the consultant Barnett Waddingham advises one scheme to sell close to 20 per cent of its assets in spite of the uncertainty surrounding its finances.

Pensions are continuing to sell return-seeking assets — including property exposures, corporate debt and private credit — and replacing them with cash and gilts, in order to prepare for liquidity demands. They are trying to avoid being forced to sell private assets at a substantial discount.

All of this is to get their portfolios in order before the BoE removes its support for the gilts market on October 14. “The BoE stepping in has not erased the issue,” said Dan Melley, partner at Mercer.

The BoE has signalled that it will not prolong the gilt-buying facility beyond next week, according to market participants. Kerrin Rosenberg, chief executive of Cardano, an advisory firm and investment manager, is urging the BoE not to consider that “the job is done” on October 14. “The Bank needs to be ready to take that action again, if they need to,” he says. “While the industry is able to bear more volatility that is not without limit. We know from our portfolio and from our clients that there is only a certain amount of collateral buffer.”

There could be lawsuits ahead, advisers said. And questions are being asked as to whether there was adequate regulation of the sector. The UK pensions regulator claims “the system coped” with the market turmoil last week, but MPs are to probe the watchdog over its role in supervising thousands of pension plans that were caught in the crossfire.

Investment consultants, which faced calls for more regulation after property funds were gated in the wake of the Brexit referendum, are now facing renewed scrutiny. The Financial Conduct Authority is conducting a “lessons learned” exercise with asset managers.

Meanwhile regulators, asset managers and pension schemes globally are looking at the UK as a test, trying to digest the potential implications for their own markets. “It’s been a real eye opener,” said Ariel Bazelal, fund manager at Jupiter. “Everyone’s kind of freaking out and asking: what just happened to these UK pensions with these LDI strategies? Is there someone else out there or another country that could get hit?”

But some worry that the soul-searching will not go far enough. “Managers are plugging into their models assumptions of a status quo that may well have evolved,” said Devitt. “I’m not sure whether we have just put a Band-Aid on the problem or actually structurally examined it . . . I’m not sure the mindset change is occurring quickly enough as to whether this is the right solution for the next regime. We tend to fight the last war.”

Additional reporting by Kate Beioley, Katie Martin, Caroline Binham, Owen Walker, Tommy Stubbington, Joshua Oliver, Jonathan Eley, Alex Barker and Laura Noonan

This story originally appeared on: Financial Times - Author:Harriet Agnew