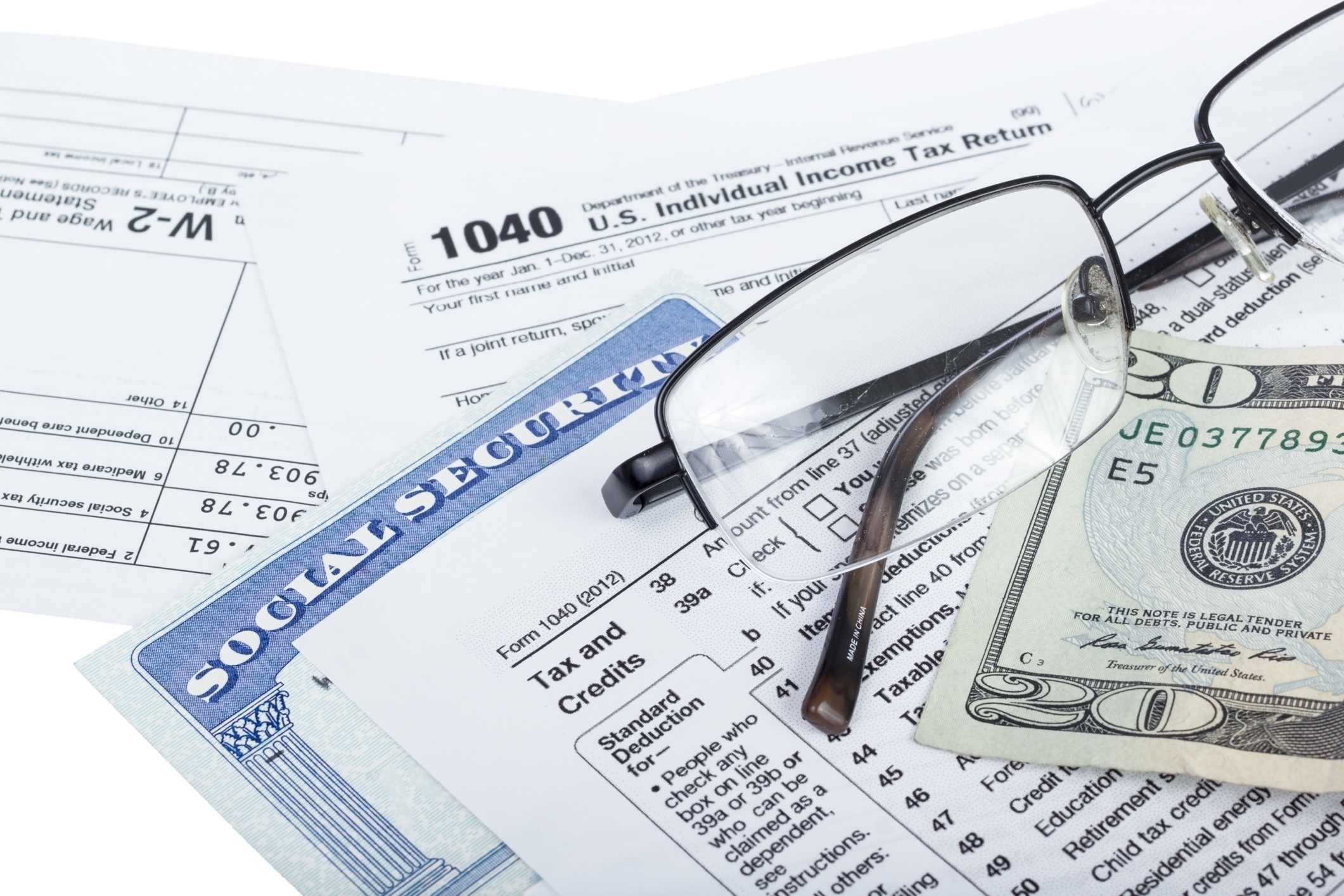

If your total income is more than $25,000 for an individual or $32,000 for a married couple filing jointly, you pay federal income on your Social Security benefits.

Join AARP for just $12 for your first year when you sign up for a 5-year term. Get instant access to members-only products and hundreds of discounts, a free second membership, and a subscription to AARP the Magazine.

If your total income is more than $25,000 for an individual or $32,000 for a married couple filing jointly, you must pay federal income taxes on your Social Security benefits. Below those thresholds, your benefits are not taxed. That applies to spousal benefits, survivor benefits and Social Security Disability Insurance (SSDI) as well as to retirement benefits.

Say you file individually, have $50,000 in income and get $1,500 a month from Social Security. You would pay taxes on 85 percent of your $18,000 in annual benefits, or $15,300. Nobody pays taxes on more than 85 percent of their Social Security benefits, no matter their income.

For purposes of determining how the Internal Revenue Service treats your Social Security payments, “income” means your adjusted gross income (line 11 of your 1040 form) plus nontaxable interest income plus half of your Social Security benefits. The IRS has an online tool that calculates how much of your benefit income is taxable.

All of the above concerns federal income taxes. Twelve states also tax Social Security to varying degrees: Colorado, Connecticut, Kansas, Minnesota, Missouri, Montana, Nebraska, New Mexico, Rhode Island, Vermont, Utah and West Virginia.

Social Security History

Background Since a pair of 1938 Treasury Department Tax Rulings, and another in 1941, Social Security benefits have been explicitly excluded from federal income taxation. (A revision was issued in 1970, but it made no changes in the existing policy.) This changed for the first time with the passage of the 1983 Amendments to the Social Security Act. Beginning in 1984, a portion of Social Security benefits have been subject to federal income taxes.

The three Treasury Rulings (see below) established as tax policy the principle that Social Security benefits were not subject to federal income taxes. This was special treatment for Social Security benefits since most private pensions are partly taxable. In most private pensions, an amount of the pension equal to the contributions made by the worker are tax-free. The amount of such private pensions which exceeds the amount of the worker's contributions, is usually subject to federal income taxes.

A slightly different, and more complicated, way of saying essentially the same thing is that the portion of pension benefits not subject to taxation is that on "after-tax income." For a worker, his entire pay is subject to federal income taxes, including that part that is subject to Social Security payroll taxes, and so, in the sometimes confusing parlance of tax policy, this is said to all be "after-tax income." His employer, however, is allowed to deduct his portion of the Social Security payroll tax from his taxable income. So Social Security payments made by the employer are considered "before-tax income" (and hence, not taxable). So the value of the "before-tax income" received by the beneficiary (i.e., the employer's contribution) is potentially taxable. Or to say it the other way, only that portion of the worker's "after-tax income" on which he paid payroll taxes, is not taxable.

Yet another way of describing this idea is to use "exclusion ratios," which is how the Treasury Department defines the taxable portion of a pension benefit. In all of these ways of describing it, the basic idea is the same: the pension recepient is generally liable for taxes on that portion of his benefits that he did not himself contribute.

Treasury's underlying rationale for not taxing Social Security benefits was that the benefits under the Act could be considered as "gratuities," and since gifts or gratuities were not generally taxable, Social Security benefits were not taxable. It is likely that Treasury took this view owing to the structure of the 1935 Act in which the taxing provisions and the benefit provisions were in separate Titles of the law. Because of this structure, one could argue that the taxes were just a form of revenue-raising, unrelated to the benefits. The benefits themselves could then be seen as a "gratuity" that the federal government paid to certain classes of citizens. Although this was clearly not true in a political and moral sense, it could be construed this way in a legal sense. In the context of public policy, most people would hold the view that the tax contributions created an "earned right" to subsequent benefits. Notwithstanding this common view, the Treasury Department ruled that there was no such necessary connection and hence that Social Security benefits were not taxable.