How banks and regulators reacted to the UK bond market meltdown

On Saturday October 8, the UK’s top bank executives were summoned to an emergency video call with Sam Woods, head of the Bank of England’s regulatory arm.

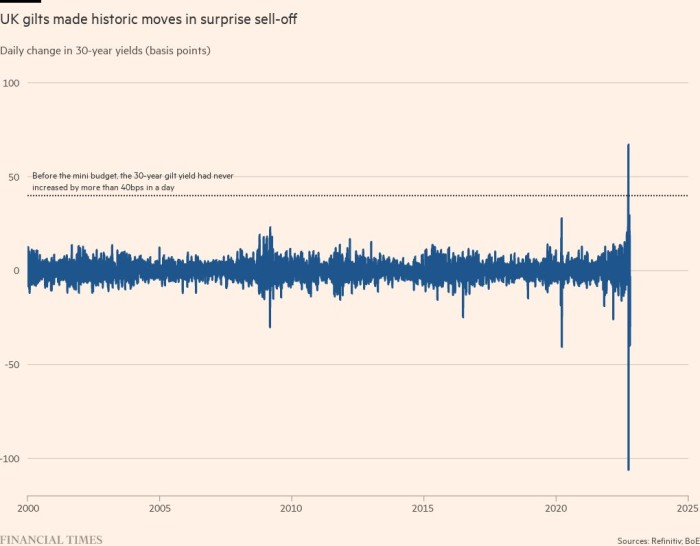

Ten days earlier the BoE had intervened in the bond market, pledging to buy up to £65bn of long-dated gilts to stabilise prices after turmoil started by Kwasi Kwarteng’s “mini” Budget and amplified by the UK’s huge pension funds.

The unprecedented fall in prices and surge in yields had taken the banks and officials by surprise.

Although the BoE’s intervention had calmed the markets, officials were still worried that the situation was fragile during their weekend meetings with senior executives at banks including Barclays, Lloyds and NatWest, along with the UK heads of JPMorgan Chase, Morgan Stanley, Goldman Sachs and Deutsche Bank. The BoE and the banks declined to comment.

For several days the banks had been providing the BoE with daily reports on their exposure to the wobbling pension funds, including information on whether the schemes were failing to meet margin calls.

British defined benefit pension funds invest heavily in gilts and also use derivatives as part of so-called liability-driven investment strategies. As gilt prices tumbled after the government’s announcement of unfunded tax cuts, the schemes were forced to sell assets — including gilts — to raise cash for margin calls from banks on the derivatives. Those sales would make gilt prices fall further, fuelling a price spiral.

Until the BoE’s intervention there was the risk of default from individual pension schemes and pooled LDI funds, operated by asset managers such as Legal and General Investment Management.

That left the banks exposed but the BoE was also interested in other routes of potential contagion, including banks’ use of reverse repo, or repurchase agreements, where they lend cash to pension funds through their corporate treasuries and take government bonds as collateral.

Among the UK lenders, Lloyds Banking Group had the largest exposure to the repo market, with £52bn, or 8.5 per cent of the assets on its corporate balance sheet. Out of the £400bn gilts repo market, as estimated by the BoE, Lloyds accounted for around 13 per cent of assets.

By comparison, NatWest had £25.8bn of repo exposure, or 6 per cent of its balance sheet assets; Santander’s UK bank had £12.6bn (4.4 per cent); HSBC’s UK bank had £8bn (2.3 per cent) and Barclays had £3.2bn (0.4 per cent).

“Lloyds definitely have one of the larger repo books, so they would have been one of the larger affected counterparties,” said a trader at a rival bank.

While the BoE was monitoring the potential knock-on effects for the banks, its focus was on the pension funds themselves and their efforts to overhaul their portfolios in the face of multibillion-pound margin calls.

By October 4, a week after the BoE’s intervention, it was becoming clear that although the central bank was willing to buy up to £5bn of gilts a day, the facility was not being used heavily. In the first six days of the programme, the BoE had purchased just £3.7bn in total.

At 7am on Monday October 10 — following its weekend of calls with bank bosses — the BoE announced it would drastically expand its support for the pensions market, increasing its capacity for buying gilts and accepting a wider range of assets as collateral for lending. A day later, it extended its bond buying to include index-linked gilts, whose value is linked to inflation.

“The really violent swings are probably behind us after the reaction from the bank,” said a chief executive who was on the calls over the weekend. “But we’re in the middle of this. Things are still moving around.”

Additional reporting by Emma Dunkley, Siddharth Venkataramakrishnan, Harriet Agnew, Stephen Morris and Joshua Franklin

This story originally appeared on: Financial Times - Author:Dan McCrum